News & Events

May

2019

14

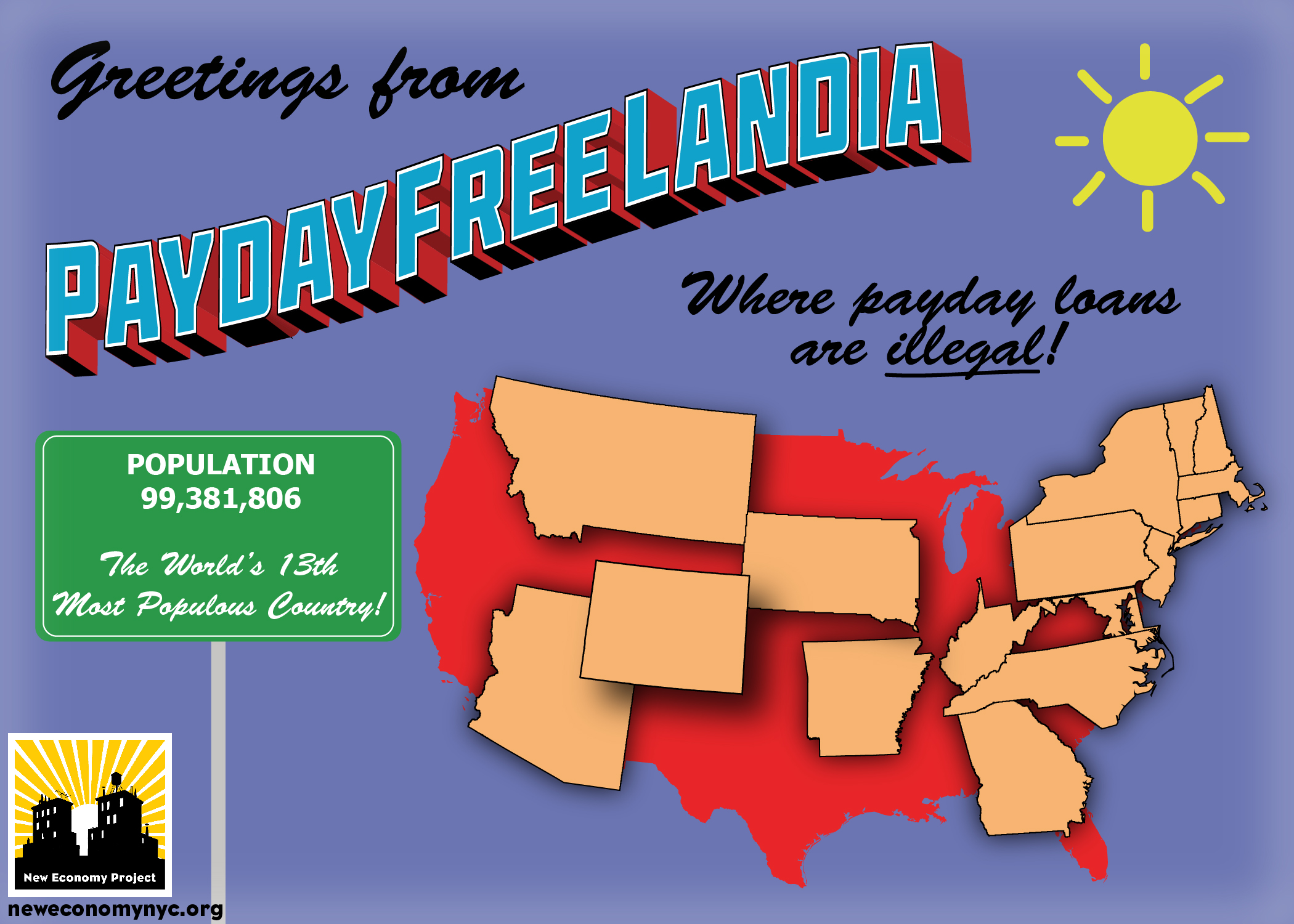

Greetings from Paydayfreelandia!

ADVOCATES FROM STATES THAT BAN PREDATORY PAYDAY LENDING EMPHATICALLY OPPOSE CFPB’S PROPOSAL TO GUT FEDERAL RULE

LISTEN TO PRESS BRIEFING:

WASHINGTON, D.C. – Today advocates from states across the country that ban predatory payday lending voiced strong opposition to the Consumer Financial Protection Bureau (CFPB)’s actions to gut federal rules to curb predatory payday lending. On a telephone briefing this morning and in comment letters submitted today to the CFPB, they presented evidence refuting the CFPB’s claim that insufficient evidence was submitted to justify the landmark rule on payday and car title lending finalized by the Bureau in 2017 and scheduled to go into effect later this year. In February, Trump-appointed director Kathy Kraninger announced a proposal to undo the rule by removing the requirement that payday and car title lenders base loans on borrowers’ ability to repay, a fundamental principle of responsible lending. Public comments close on that proposal today.

Paydayfreelandia is a coalition of community, civil rights, labor, and faith-based groups, as well as community development financial institutions, from states that prohibit predatory payday lending. Paydayfreelandia includes 16 states, plus D.C., and is home to 100 million people. Laws banning predatory payday lending in these states ensure that families are not subjected to the devastating payday lending debt cycle, which often leads to financial insolvency, overdraft fees, closed bank accounts and bankruptcy. Advocates cited the billions of dollars preservedin their states, thanks to their strong laws.

Members of the coalition made the following comments:

“New York long ago banned payday lending, so we know that no one needs payday loans, which exploit people who are struggling financially,” said Sarah Ludwig, founder and co-director of New Economy Project, based in New York City. “The CFPB’s proposal is part of the Trump administration’s dangerous effort to deregulate financial services. It is cynically meant to enrich the predatory lending industry — at tremendous cost to people and communities of color, immigrants, women, older adults, and low-income people, in particular.”

“It is the CFPB’s job to protect consumers from harmful financial products. They should do their job,” said Rabbi David Rosenn, Executive Director of the Hebrew Free Loan Society, a nonprofit lender based in New York City. “When these regulatory agencies put rules in place, they do it to protect Americans from likely harm. When they undo the rules and let industries regulate themselves on the most basic safety issues, people tend to get hurt. That’s why it’s so baffling that after a painstaking process that led to some very basic rules to prevent risky and abusive lending, the CFPB now wants to claim those rules are no longer necessary. The rules are necessary. The CFPB said so itself, and nothing has changed in the short time since it arrived at that conclusion.”

“Although Pennsylvania has never legalized these loans, payday lenders employed a variety of schemes in the past to set up shops in our communities. Fortunately, courts and regulators effectively stopped debt-trap lending, bringing relief to consumers in our state,” said Kerry Smith, Senior Staff Attorney with Community Legal Services of Philadelphia. “Having once seen the harms of payday lending, we know that families in Pennsylvania are better off without these unaffordable, predatory loans. That’s why we have been working with a broad coalition to keep our state law strong, and why the CFPB should keep its national rule for states without interest rate caps.”

“At its core, the CFPB Rule in its current form establishes a strong ability-to-repay standard, a fundamental tenet of responsible lending practices. Our experience demonstrates that people are better off without these harmful, high-cost, unaffordable loans,” said Berneta Haynes, Senior Director of Policy and Access at Georgia Watch. “While Georgia has a ban on payday lending, our citizens still face the debt trap caused by car title loans. This is particularly detrimental to Georgia’s 681,840 veterans and communities of color, populations that car title lenders target and exploit. The rule in its current form is critically important to preventing the harms of this predatory business model and stopping the debt trap.”

“The ability-to-repay rule is a common sense and reasonable requirement that protects borrowers from taking on loans they cannot afford and from falling into debt traps with crippling fees and interest rates,” said Beverly Brown Ruggia, Financial Justice Organizer for New Jersey Citizen Action. “The decision to rescind the rule is an example of the CFPB’s new and overt mission under Director Kraninger to protect maximum profits for financial companies regardless of the devastating harm they cause consumers.”