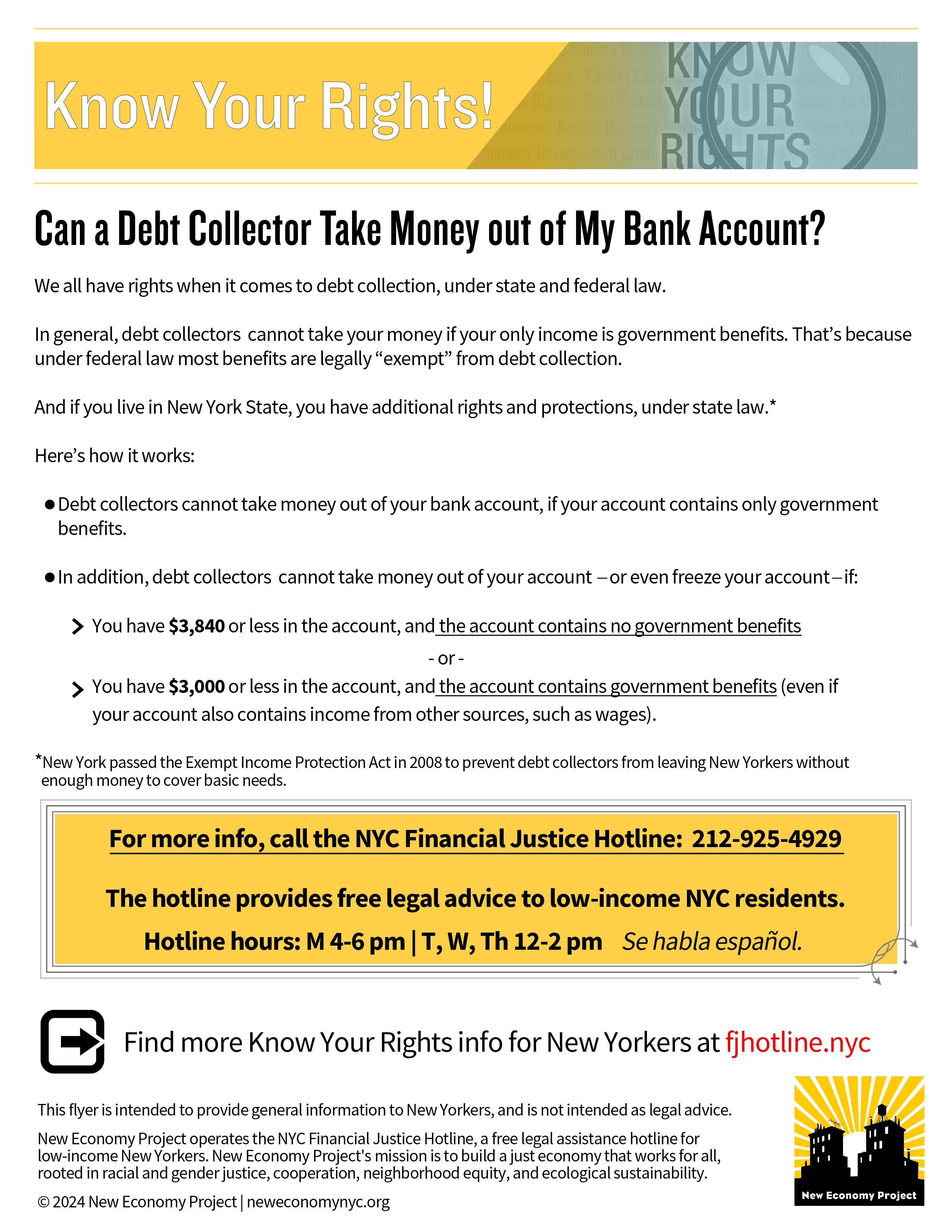

Frozen Bank Accounts

IMPORTANT NOTE: The information on this page applies to accounts that have been frozen because of private debts like credit cards, medical bills, and bank loans. If you have child support debt, or if you owe money to the government for taxes or a student loan, different rules apply.

What is a frozen bank account?

A frozen bank account is a bank account that you cannot access because a creditor has placed a restraint on it. When your bank account is frozen, you can put money into it, but you can’t take money out.

Why is my bank account frozen?

A frozen bank account is a sure sign that a creditor or debt collector has obtained a court judgment against you (or your joint account holder, if you have a joint bank account). A creditor or debt collector cannot freeze your bank account unless it has a judgment. Judgment creditors freeze people’s bank accounts as a way of pressuring people to make payments.

Why does my frozen bank account have a very large negative balance?

A judgment creditor typically puts a hold on your bank account for twice the amount of the judgment against you. This hold shows up on your bank account as a negative balance. You do not actually owe all of this money to the judgment creditor. Rather, the amount you owe is the amount of the judgment.

Does my bank have to give me notice before freezing my account?

No. Unfortunately, the law provides that when the bank receives a restraining notice, it must freeze your account immediately, before notifying you. That is why most people discover that their account is frozen when they try to use their ATM cards and they suddenly do not work.

Does a judgment creditor have to give me notice before freezing my account?

A judgment creditor does not have to give you specific notice before freezing your bank account. However, a creditor or debt collector is required to notify you (1) that it has filed a lawsuit against you; and (2) that it has obtained a judgment against you. If your first notice of the court case is a frozen bank account, you have not received proper notice under the law.

Do I need a lawyer to unfreeze my bank account?

No. Thousands of New Yorkers have successfully obtained release of their bank accounts without a lawyer.

How do I unfreeze my bank account?

The best way to unfreeze your bank account is to erase the judgment against you. This is called “vacating” the judgment. Once the judgment is vacated, your account will be released automatically. A creditor or debt collector has no right to freeze your account without a judgment. For step by step instructions, see Vacating a Default Judgment.

Can I negotiate a settlement to get my bank account released without going to court?

If your bank account contains exempt benefits such as Social Security, you do not need to negotiate a settlement in order the lift the lien. See below for more information.

If your bank account contains recent wages or nonexempt funds, it is probably in your best interest to go to court. Most of our clients find that they can negotiate a much better deal in court than they can outside of court. For this reason, we strongly recommend that you go to court and vacate the default judgment, if at all possible. There are many good reasons to try to vacate the judgment. In New York State, unpaid judgments are collectible for up to 20 years. Having an unpaid judgment exposes you to repeated efforts to freeze your bank account and/or garnish your wages. Judgments also appear on your credit report, where they affect your ability to get loans, employment, and housing. In most cases, you need to have the judgment vacated in order to clear it from your credit report. Therefore, for your own protection, you are almost always better off getting the judgment vacated instead of settling outside of court.

What if my frozen bank account contains only funds that are exempt from debt collection, like Social Security?

If all the funds in your bank account are exempt from debt collection, a judgment creditor has no right to hold onto the account, and must release it immediately, even if it has a judgment against you. To obtain release of your account, you need to call the judgment creditor’s attorney (you can get the attorney’s contact information from your bank). Notify the attorney that all the funds in your bank account are exempt from debt collection and demand an immediate release of your account. The attorney may ask you to fax or mail proof of your exempt income. You can send up to three months of bank statements as proof (feel free to redact your bank statements to protect your privacy – the attorney only needs to see deposits, not purchases). Please be aware that the judgment creditor’s attorney may delay and make excuses to avoid releasing your exempt funds. If you have any trouble at all, you should follow our instructions to vacate the default judgment. In general, even when you have exempt funds, you are better off vacating the judgment if at all possible.

What if my frozen bank account contains some funds that are exempt and some funds that are NOT exempt?

This situation is also known as “having comingled funds.” In this scenario, your exempt funds are still exempt from collection, even though they are mixed with other, non-exempt funds. However, even though your funds are still exempt, it is often difficult to persuade a debt collector to release your account. Rather than argue with the debt collector on the phone, we advise you to go to court and vacate the default judgment as soon as possible in order to obtain the fastest release of your account.

Can a judgment creditor actually take money from my bank account?

Yes. A creditor or debt collector can hire a New York City Marshal to levy funds from your account.

How long will a judgment creditor wait before seizing my funds?

There is no set time limit. Some judgment creditors try to seize funds right away, and others never actually take funds at all. Most judgment creditors will wait at least a few weeks before attempting to levy your bank account.

If a debt collector levies my bank account, can I get my money back?

Yes. You should go to court and try to vacate the default judgment. As part of this process, you can ask the court to order the creditor or debt collector to return your funds.

What if I have a joint bank account?

The first step is to determine why the joint bank account is frozen. Usually, there is a judgment against one, but not both, joint account holders. Telephone the attorney for the judgment creditor and ask for information about the case, including the court, the index number, and the name of the defendant(s).

If there is a judgment against you, you can obtain release of the account by following the steps to vacate the default judgment. If the account contains only exempt income (for example, your mother’s pension or your child’s SSI), you should also telephone the attorney to obtain release of the exempt funds, as described above.

If your account is frozen because of a judgment against someone else, it is best for the other person to vacate the default judgment, if at all possible. If this proves to be impossible, you also have the right to file court papers to obtain release of your account.

-

Under Banking Law 678 , if you can prove that you added the other person to your account for convenience only, your entire account will be released. You must prove that you did not intend to give the joint account holder the right to own half of the money in the account. You can show that the joint account is for your convenience only by demonstrating that you are the only person who used the account, that the other person did not have an ATM card or withdrawal privileges, or by providing other information that tends to show that the account actually belongs to you alone. You can also ask your bank to write a letter stating that the joint account was for purposes of convienence only.

-

If you cannot prove that the joint account is for convenience only, then you can recover half of the money that is in the account. Under Banking Law 675, the judgment creditor cannot have more than half the money in the account unless it proves that the money belongs to the other person, and not to you. This is because the law presumes that half the money in the account belongs to you and half belongs to the other person.

More Information

How to Read a Civil Court Summons (PDF)

The Basics of Defending Creditor Lawsuits

Common Defenses to Creditor Lawsuits

Negotiating A Settlement Agreement in Court

What is Exempt from Debt Collection?

Helpful Links and Resources

LawHelp/NY: attorney referrals and information for pro se litigants

National Association of Consumer Advocates: national database of consumer lawyers

New York City Civil Court: information about representing yourself in court, including contact information and court forms

eCourts: information about cases filed in New York courts

Laws of New York: complete text of New York laws

Disclaimer: This site provides general information for consumers and links to other sources of information. This site does not provide legal advice, which you can only get from an attorney. New Economy Project has no control over the information on linked sites.

Copyright ©2007 by the Neighborhood Economic Development Advocacy Project, Inc.

All Rights Reserved